New 2026 Healthcare Benefits: A Comparison of 3 Plans to Optimize Your Coverage

Navigating the Future: A Deep Dive into New 2026 Healthcare Benefits and Plan Comparisons

The landscape of healthcare is in a perpetual state of evolution, with significant changes often introduced each year that can profoundly impact individuals, families, and employers alike. As we look ahead to 2026, a new wave of healthcare benefits and policy adjustments is on the horizon, promising both new opportunities and potential challenges for those seeking comprehensive and affordable coverage. Understanding these impending changes, particularly through a meticulous 2026 Healthcare Benefits Comparison, is not merely a recommendation—it’s an absolute necessity for optimizing your health coverage and safeguarding your financial well-being. This extensive guide aims to provide a thorough examination of the new 2026 healthcare benefits, offering a detailed comparison of three distinct plan archetypes to help you make informed decisions.

The decisions made regarding healthcare coverage are among the most critical an individual or family will face. It’s not just about finding a plan; it’s about finding the right plan that aligns with your health needs, financial situation, and lifestyle. With the complexities surrounding deductibles, premiums, co-pays, out-of-pocket maximums, and network restrictions, the task can often feel daunting. However, by breaking down the key aspects of the new 2026 offerings and comparing them systematically, we can demystify the process and empower you to choose with confidence. Our focus will be on providing actionable insights, highlighting the pros and cons of each plan type, and offering strategic advice on how to leverage the new benefits to your advantage.

The Shifting Tides of Healthcare: What to Expect in 2026

Before delving into specific plan comparisons, it’s crucial to grasp the broader context of what 2026 might bring to the healthcare sector. Several factors typically influence changes in healthcare benefits, including legislative reforms, advancements in medical technology, shifts in population health trends, and economic conditions. While specific legislative details for 2026 are still firming up, historical patterns suggest an ongoing emphasis on affordability, accessibility, and quality of care. We anticipate continued discussions around prescription drug costs, mental health parity, and the expansion of telehealth services.

Key Trends and Anticipated Changes for 2026:

- Increased Focus on Preventive Care: Expect an even greater emphasis on preventive services, with many plans potentially expanding coverage for screenings, vaccinations, and wellness programs designed to keep individuals healthier and reduce long-term costs.

- Telehealth Integration: The accelerated adoption of telehealth during recent years is likely to solidify, with more plans offering robust virtual care options, potentially including mental health counseling and chronic disease management via remote platforms.

- Prescription Drug Reform: Discussions and potential legislation aimed at lowering prescription drug costs for consumers are expected to continue, which could lead to changes in formulary designs and out-of-pocket expenses.

- Mental Health Parity: The push for equitable coverage of mental health and substance abuse services compared to physical health services will likely remain a priority, leading to improved access and reduced cost barriers for these essential services.

- Personalized Healthcare Approaches: With advancements in data analytics and genetic understanding, some plans may begin to offer more personalized health management tools and benefits tailored to individual risk factors and health profiles.

- Employer-Sponsored Plan Adjustments: Employers will continue to navigate rising healthcare costs, potentially leading to adjustments in their offered plans, including increased cost-sharing or a wider array of plan choices to accommodate diverse employee needs.

Understanding these overarching trends provides a foundational understanding for our 2026 Healthcare Benefits Comparison. It helps contextualize why certain plan features might become more prevalent or why specific benefits might see enhancements or limitations.

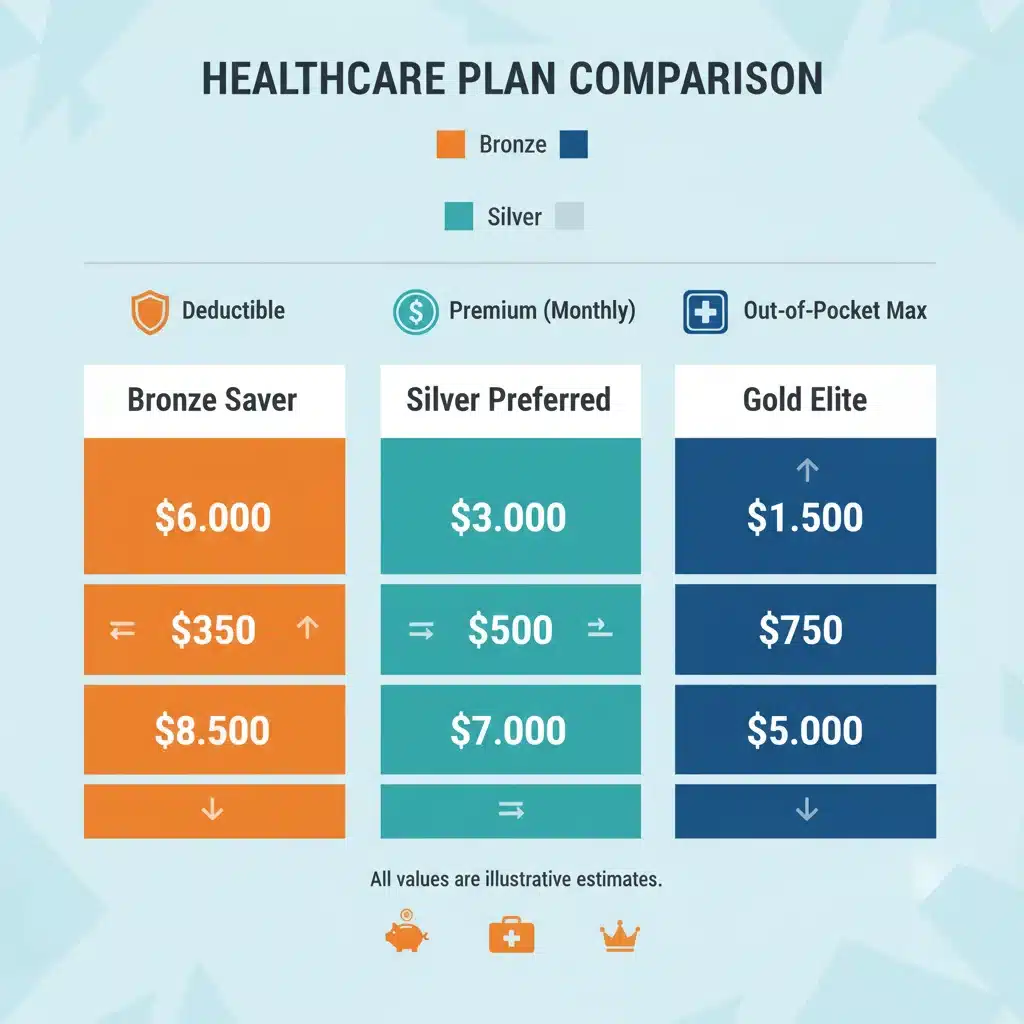

Plan Archetype 1: The High-Deductible Health Plan (HDHP) with Health Savings Account (HSA)

High-Deductible Health Plans (HDHPs) paired with Health Savings Accounts (HSAs) have grown immensely in popularity over the past decade, especially for individuals and families who are relatively healthy and seek lower monthly premiums. This plan type is often a cornerstone of any comprehensive 2026 Healthcare Benefits Comparison due to its unique financial structure and tax advantages.

How HDHP/HSA Plans Work:

An HDHP is characterized by a higher annual deductible than traditional plans. This means you pay more out-of-pocket for medical services before your insurance coverage begins to pay. However, this higher deductible is typically offset by significantly lower monthly premiums. The "HSA-eligible" component is crucial: it allows you to open a Health Savings Account, a tax-advantaged savings account that can be used for qualified medical expenses.

Pros of HDHP/HSA in 2026:

- Lower Monthly Premiums: For many, the most attractive feature is the reduced monthly cost, which can lead to substantial savings over the year if medical needs are minimal.

- Tax Benefits: Contributions to an HSA are often tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free. This "triple tax advantage" makes HSAs a powerful financial tool.

- Portability: HSAs are owned by the individual, not the employer or insurance company. This means the account and its funds go with you if you change jobs or health plans.

- Investment Potential: Once a certain balance is reached, many HSAs allow you to invest the funds, similar to a 401(k) or IRA, offering long-term growth potential for future healthcare costs in retirement.

- Empowerment and Cost Awareness: Because you’re paying more out-of-pocket initially, HDHPs often encourage consumers to be more proactive in understanding healthcare costs and seeking value-based care.

Cons of HDHP/HSA in 2026:

- High Upfront Costs: If you experience an unexpected illness or injury early in the year, you could face significant out-of-pocket expenses before your deductible is met.

- Requires Financial Discipline: Maximizing the benefits of an HSA requires consistent contributions and careful management of funds.

- Not Ideal for High Medical Needs: Individuals with chronic conditions or frequent medical appointments may find themselves consistently paying high out-of-pocket costs, potentially negating the savings from lower premiums.

- Complexity: The interplay between the HDHP and HSA can be confusing for some, requiring a solid understanding of how both components work together.

When considering an HDHP/HSA for your 2026 Healthcare Benefits Comparison, evaluate your typical medical expenses, your ability to comfortably cover the deductible, and your financial strategy for long-term health savings.

Plan Archetype 2: The Traditional Preferred Provider Organization (PPO) Plan

The Preferred Provider Organization (PPO) plan remains one of the most popular and widely adopted healthcare options, prized for its flexibility and broad network access. It’s a crucial component in any thorough 2026 Healthcare Benefits Comparison, especially for those who value choice and don’t want to be tied to a primary care physician (PCP) for referrals.

How PPO Plans Work:

PPO plans offer a network of "preferred" providers (doctors, hospitals, specialists) with whom the insurance company has negotiated discounted rates. You are generally not required to choose a primary care physician (PCP) or obtain referrals to see specialists. You can also see out-of-network providers, though at a higher cost-sharing amount.

Pros of PPO Plans in 2026:

- Flexibility and Choice: This is arguably the biggest advantage. PPO plans offer a wide range of doctors and hospitals to choose from, both in-network and, with higher cost-sharing, out-of-network.

- No Referrals Needed: You typically don’t need a referral from a PCP to see a specialist, streamlining access to specialized care.

- Predictable Co-pays: Many services, especially office visits, come with a predictable co-pay after meeting your deductible, making budgeting for routine care easier.

- Good for Frequent Users of Healthcare: If you anticipate needing to see specialists often or prefer the freedom to choose your providers, a PPO can offer peace of mind.

- Broader Networks: PPO networks are often larger than those of other plan types, which can be beneficial if you travel frequently or live in an area with fewer in-network options for other plans.

Cons of PPO Plans in 2026:

- Higher Monthly Premiums: The increased flexibility and broader network typically come at a cost, meaning PPO plans often have higher monthly premiums compared to HDHPs or HMOs.

- Higher Deductibles (compared to HMOs): While not as high as HDHPs, PPO deductibles can still be substantial, and you’ll need to meet this before your plan pays a significant portion of costs.

- Out-of-Network Costs: While you have the option to go out-of-network, the cost-sharing (deductibles, co-insurance) for these services is significantly higher, potentially leading to large unexpected bills.

- Balance Billing: Out-of-network providers may "balance bill" you for the difference between what your insurance pays and the provider’s total charge, which can be considerable.

For your 2026 Healthcare Benefits Comparison, a PPO plan might be ideal if you prioritize choice, flexibility, and direct access to specialists, and are willing to pay higher premiums for these benefits.

Plan Archetype 3: The Health Maintenance Organization (HMO) Plan

Health Maintenance Organization (HMO) plans represent another significant category in the healthcare landscape, often favored for their lower out-of-pocket costs and emphasis on coordinated care. They are an essential consideration in any thorough 2026 Healthcare Benefits Comparison, particularly for those who prefer a structured approach to their healthcare management and appreciate cost predictability.

How HMO Plans Work:

HMO plans typically require you to choose a primary care physician (PCP) within the plan’s network. Your PCP acts as a "gatekeeper," coordinating all your medical care, including referrals to specialists. With an HMO, you generally must receive care from providers within the plan’s network, except in emergencies, or the services may not be covered at all.

Pros of HMO Plans in 2026:

- Lower Monthly Premiums: HMOs often boast the lowest monthly premiums among the three plan types, making them an attractive option for budget-conscious individuals and families.

- Lower Out-of-Pocket Costs: Typically, HMOs have lower deductibles, fixed co-pays for most services, and lower out-of-pocket maximums, leading to more predictable healthcare expenses.

- Coordinated Care: The PCP gatekeeper model ensures that your care is coordinated, which can be beneficial for managing chronic conditions or navigating complex medical situations. This integrated approach can lead to better health outcomes.

- Emphasis on Preventive Care: Many HMOs place a strong emphasis on preventive health, offering robust coverage for screenings and wellness programs to keep members healthy.

- Simpler Billing: With most services covered by co-pays once the (often low) deductible is met, the billing process can be less complex than with plans involving more co-insurance and out-of-network charges.

Cons of HMO Plans in 2026:

- Limited Provider Choice: The biggest drawback is the restricted network. You must choose providers within the HMO’s network, and seeing an out-of-network provider (outside of emergencies) means little to no coverage.

- Referral Requirements: Needing a referral from your PCP to see a specialist can add an extra step and potential delay to accessing specialized care.

- Less Flexibility: If you travel frequently or have specific preferred doctors outside the HMO network, this plan type can be restrictive.

- Changing PCPs: If you’re unhappy with your PCP, changing can sometimes be a bureaucratic process.

For your 2026 Healthcare Benefits Comparison, an HMO plan could be an excellent choice if you prioritize lower costs, predictable expenses, and don’t mind working within a defined network, with your PCP coordinating your care.

Making Your Decision: A Strategic Approach to 2026 Healthcare Benefits

Choosing the right healthcare plan for 2026 is a highly personal decision that requires careful consideration of various factors. There is no one-size-fits-all answer, and what works best for one individual or family may not be suitable for another. Use this detailed 2026 Healthcare Benefits Comparison as a starting point, but always dig deeper into the specifics of any plan you consider.

Factors to Consider When Comparing Plans:

- Your Health Needs and Usage Patterns:

- Do you have chronic conditions that require frequent specialist visits or ongoing prescriptions?

- Are you generally healthy and only expect to need preventive care?

- Do you anticipate any major medical procedures or life events (e.g., pregnancy) in 2026?

- How often do you visit the doctor or require urgent care?

- Financial Situation and Budget:

- What can you comfortably afford in monthly premiums?

- Do you have an emergency fund to cover a high deductible if unexpected medical needs arise?

- Are you able to contribute regularly to an HSA to maximize its tax benefits?

- What are your tolerance levels for out-of-pocket expenses?

- Provider Preferences and Network Access:

- Are your current doctors and specialists in-network for the plans you are considering?

- Is it important for you to have the flexibility to see any doctor, even out-of-network?

- Do you prefer the coordinated care model of an HMO, or the self-directed approach of a PPO?

- How important is direct access to specialists without referrals?

- Prescription Drug Coverage:

- Review the formulary (list of covered drugs) for each plan to ensure your necessary medications are covered and at what tier.

- Understand the co-pays or co-insurance for different drug tiers.

- Ancillary Benefits:

- Does the plan offer vision, dental, or other wellness programs that are important to you?

- Are there mental health and substance abuse services that meet your potential needs?

Practical Steps for Your 2026 Healthcare Benefits Comparison:

- Gather Information: Collect detailed summaries of benefits and coverage (SBCs) for each plan you’re considering. These documents are standardized and make direct comparisons easier.

- Calculate Total Potential Costs: Don’t just look at premiums. Estimate your total annual out-of-pocket costs, including deductibles, co-pays, and co-insurance, based on your anticipated medical usage. Consider the maximum out-of-pocket limit for each plan.

- Verify Provider Networks: Use the plan’s online provider directory to confirm that your preferred doctors, specialists, and hospitals are in-network. This is especially critical for HMOs.

- Check Prescription Drug Coverage: Input your regular prescriptions into the plan’s formulary search tool to see coverage and estimated costs.

- Utilize Employer Resources: If enrolling through an employer, attend information sessions and speak with HR or benefits administrators. They can provide valuable insights and answer specific questions.

- Seek Expert Advice: If you’re still unsure, consider consulting with a licensed insurance broker or financial advisor who specializes in healthcare planning.

The Role of Preventative Care and Wellness Programs in 2026 Healthcare

As part of the evolving 2026 Healthcare Benefits Comparison, it’s increasingly important to highlight the significant role that preventative care and wellness programs play. Modern healthcare is shifting from a purely reactive model (treating illness) to a more proactive one (preventing illness and promoting well-being). Many 2026 plans are expected to reflect this shift, offering enhanced benefits that support a healthier lifestyle.

Why Preventative Care Matters:

- Early Detection: Regular screenings (e.g., mammograms, colonoscopies, blood pressure checks) can detect potential health issues early, when they are often more treatable and less costly.

- Disease Prevention: Vaccinations, lifestyle counseling, and health education can prevent the onset of many diseases.

- Cost Savings: Investing in preventive care can significantly reduce the need for more expensive treatments down the line, benefiting both individuals and the healthcare system.

- Improved Quality of Life: Staying proactive about your health leads to a better overall quality of life, with fewer health disruptions.

Wellness Programs in 2026:

Many 2026 healthcare plans, particularly those offered by employers, may include or enhance wellness programs. These can range from fitness challenges and smoking cessation programs to nutritional counseling and stress management workshops. Some plans might offer incentives, such as reduced premiums or gift cards, for participation and achieving health goals. When conducting your 2026 Healthcare Benefits Comparison, inquire about these programs, as they can add considerable value beyond basic medical coverage.

Understanding the “Out-of-Pocket Maximum”

One of the most critical figures to understand in any healthcare plan, and particularly when conducting a 2026 Healthcare Benefits Comparison, is the “out-of-pocket maximum.” This figure represents the absolute most you will have to pay for covered medical services in a given plan year. Once you reach this limit, your insurance plan will pay 100% of all covered medical expenses for the remainder of the year.

What Counts Towards Your Out-of-Pocket Maximum?

Generally, the following contributions count towards your out-of-pocket maximum:

- Deductibles: The amount you pay before your insurance starts to cover costs.

- Co-payments (Co-pays): A fixed amount you pay for a covered service, like a doctor’s visit.

- Co-insurance: Your share of the cost of a covered service, calculated as a percentage (e.g., after your deductible, your plan might pay 80% and you pay 20%).

What typically does NOT count towards your out-of-pocket maximum:

- Monthly Premiums: The regular payment you make to keep your coverage active.

- Non-covered Services: Costs for services that your plan does not cover.

- Out-of-Network Charges (for PPOs): If you go out-of-network with a PPO, only a portion of what the insurer deems “reasonable and customary” may count, and balance billing charges will not.

The out-of-pocket maximum acts as a financial safety net, protecting you from catastrophic medical bills. When you perform your 2026 Healthcare Benefits Comparison, comparing this figure across different plans is just as important as comparing premiums and deductibles, especially if you have concerns about potential high medical costs.

Conclusion: Empowering Your 2026 Healthcare Choices

The journey through the new 2026 healthcare benefits landscape may seem intricate, but with a structured approach and a clear understanding of your options, it becomes a path to optimized coverage. Our detailed 2026 Healthcare Benefits Comparison of HDHP/HSA, PPO, and HMO plans highlights that each plan type has distinct advantages and disadvantages, catering to different needs, preferences, and financial situations.

Remember, the goal is not just to have "a" health insurance plan, but to have the "best" health insurance plan for you. This means carefully evaluating your personal and family health needs, assessing your financial resources, and considering your comfort level with different levels of flexibility and cost-sharing. As 2026 approaches, take the time to:

- Review your current health status and anticipated medical needs.

- Analyze your budget for monthly premiums and potential out-of-pocket expenses.

- Investigate the networks of potential plans to ensure your preferred providers are included.

- Understand the specifics of prescription drug coverage.

- Leverage all available resources, including employer benefits administrators and official plan documents.

By diligently performing your own 2026 Healthcare Benefits Comparison, you empower yourself to make a confident and informed decision, securing the optimal healthcare coverage that protects your health and financial future. The proactive steps you take today will lay the foundation for a healthier and more secure tomorrow. Don’t leave your health coverage to chance; take control and choose wisely for 2026.