Credit Score Optimization in 2026: 3 Key Actions to Boost Your FICO Score by 50 Points in 6 Months

In the evolving financial landscape of 2026, your FICO score remains a cornerstone of your financial health. A higher FICO score unlocks doors to better interest rates on loans, advantageous credit card offers, lower insurance premiums, and even smoother rental applications. If you’re looking to significantly improve your financial standing, focusing on credit score optimization is paramount. This comprehensive guide will walk you through three crucial actions you can take right now to boost your FICO score by a remarkable 50 points in just six months.

Many people view their credit score as a static number, a consequence of past financial decisions. However, with strategic effort and consistent habits, your credit score is highly dynamic and can be improved significantly. We’re not talking about quick fixes or dubious credit repair schemes. Instead, we’re focusing on legitimate, impactful strategies that leverage the very algorithms FICO uses to calculate your score. By understanding these mechanisms, you can proactively engage in credit score optimization to reshape your financial future.

The journey to a 50-point FICO increase in six months requires dedication and a clear understanding of what influences your score. We’ll delve into the foundational elements of FICO scoring and then provide actionable steps that target the most impactful areas. Get ready to transform your credit profile and open up new financial possibilities.

Understanding Your FICO Score: The Foundation of Credit Score Optimization

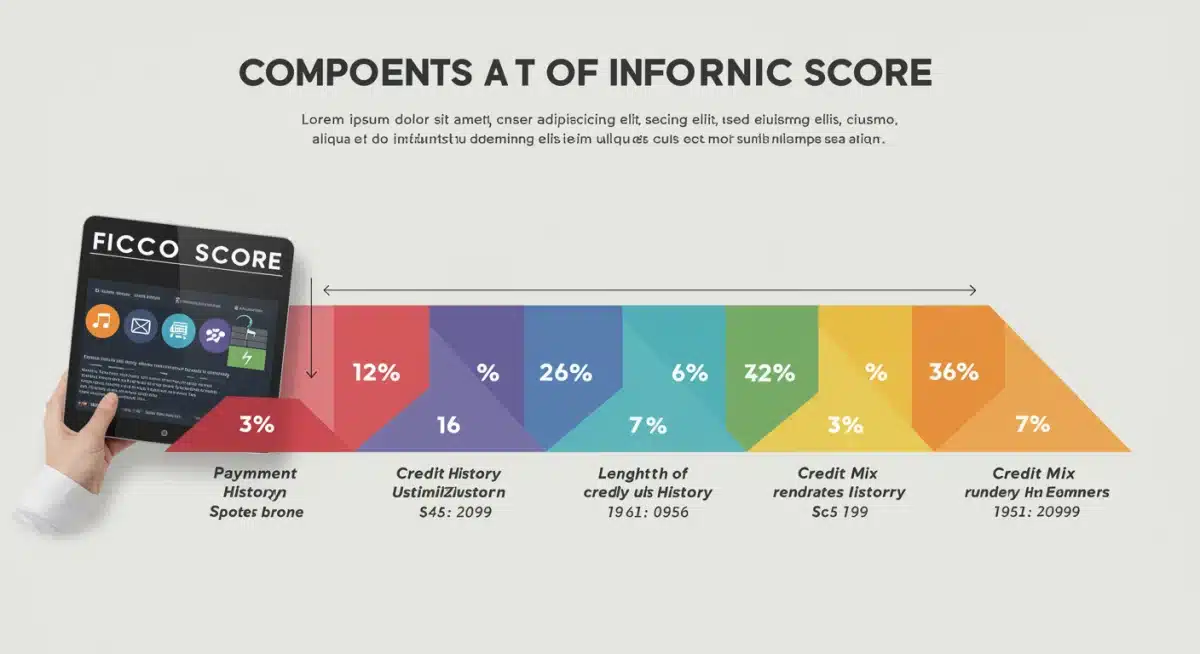

Before we dive into specific actions, it’s crucial to understand what makes up your FICO score. FICO, or Fair Isaac Corporation, uses a complex algorithm to assess your creditworthiness. While the exact formula is proprietary, FICO openly shares the primary categories and their approximate weightings in determining your score. Knowing these components is the first step in effective credit score optimization:

- Payment History (35%): This is the most significant factor. It reflects whether you pay your bills on time. Late payments, bankruptcies, and collections accounts can severely damage your score. Consistent on-time payments are the bedrock of a good credit score.

- Amounts Owed / Credit Utilization (30%): This factor looks at how much of your available credit you are using. A high credit utilization ratio (the amount of credit you’re using compared to your total available credit) signals higher risk and can lower your score. Keeping this ratio low is a key aspect of credit score optimization.

- Length of Credit History (15%): Generally, the longer your credit accounts have been open and in good standing, the better. This demonstrates a proven track record of responsible credit management.

- New Credit (10%): Opening too many new credit accounts in a short period can be seen as risky. Each hard inquiry can temporarily ding your score.

- Credit Mix (10%): Having a healthy mix of different types of credit (e.g., credit cards, installment loans like mortgages or car loans) can positively impact your score, showing you can handle various forms of credit responsibly.

With these components in mind, our three key actions for credit score optimization will strategically address the areas that offer the most significant potential for improvement within a six-month timeframe.

Action 1: Master Your Payments and Reduce Credit Utilization (65% of Your Score!)

This single action targets two of the most heavily weighted categories of your FICO score: payment history (35%) and amounts owed (30%). By focusing intensely on these areas, you can achieve substantial gains in your FICO score quickly. This is where the most impactful credit score optimization happens.

Sub-Action 1.1: Never Miss a Payment Again

This might seem obvious, but its importance cannot be overstated. A single 30-day late payment can drop your score by dozens of points, and its impact can linger for years. To achieve a 50-point increase, absolutely no late payments can occur during your six-month optimization period.

- Set Up Automatic Payments: This is the simplest and most effective way to ensure you never miss a due date. Most banks and credit card companies offer this service. Set it to pay at least the minimum amount, or ideally, the full statement balance.

- Calendar Reminders: Even with auto-pay, it’s wise to have calendar alerts a few days before due dates as a backup.

- Prioritize Payments: If you’re struggling, prioritize minimum payments on all accounts to avoid late marks. Focus on paying down high-interest debt after ensuring all minimums are covered.

Sub-Action 1.2: Drastically Reduce Your Credit Utilization Ratio

Your credit utilization ratio is calculated by dividing your total outstanding credit balances by your total available credit limits. For example, if you have a credit card with a $10,000 limit and a $3,000 balance, your utilization for that card is 30%. The general rule of thumb for good credit health is to keep your overall utilization below 30%, but for aggressive credit score optimization, aim for under 10%.

Here’s how to achieve this:

- Pay Down Balances: This is the most direct way. Focus on cards with the highest utilization first. Even paying off a small balance can have a disproportionate positive effect if it significantly lowers that card’s utilization.

- Make Multiple Payments Per Month: Instead of waiting for the statement due date, make smaller payments throughout the month. This can keep your reported balance low, as credit card companies typically report your balance to credit bureaus once a month, often on your statement closing date. If your balance is low on that specific date, your utilization will look better.

- Request Credit Limit Increases (Cautiously): If you have a good payment history with a particular card issuer, you might request a credit limit increase. This increases your total available credit, which can lower your utilization ratio even if your balance stays the same. However, be cautious: a credit limit increase request might result in a hard inquiry, which can temporarily ding your score. Only do this if you are confident you won’t be tempted to spend more. Also, this is more effective if your payment history on that specific card is stellar.

- Avoid Closing Old Accounts: While tempting to close accounts once paid off, this reduces your total available credit and can increase your utilization ratio on remaining cards. It also shortens your length of credit history, which is another FICO factor.

Impact in 6 Months: By diligently applying these strategies, you can see a noticeable increase in your FICO score within 1-3 months, with sustained effort leading to significant gains by the six-month mark. This is the cornerstone of effective credit score optimization.

Action 2: Address Derogatory Marks and Monitor Your Credit Reports (Crucial for Accuracy)

While paying on time and reducing utilization are proactive steps, credit score optimization also involves reactive measures, particularly addressing anything that might be incorrectly dragging your score down. Errors on credit reports are surprisingly common and can severely hinder your progress.

Sub-Action 2.1: Obtain and Review Your Credit Reports Regularly

You are entitled to a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months via AnnualCreditReport.com. During your six-month optimization period, it’s advisable to pull one report every two months, rotating between the bureaus, or pull all three at the beginning and then again at the four-month mark.

- Look for Errors: Scrutinize every detail: incorrect personal information, accounts you don’t recognize, duplicate accounts, incorrect payment statuses, or accounts that should have dropped off your report due to age.

- Identify Old Debts: Note any old collections or charge-offs. These can have a significant negative impact.

Sub-Action 2.2: Dispute Inaccurate Information

If you find errors, dispute them immediately. This process can take time, so starting early in your six-month window is critical.

- Contact the Credit Bureau: You can dispute online, by mail, or by phone. Provide all supporting documentation. The bureau has 30 days (sometimes 45) to investigate.

- Contact the Creditor: It can also be helpful to contact the original creditor to inform them of the inaccuracy.

- Follow Up: Keep detailed records of all correspondence and follow up if you don’t hear back within the stipulated timeframe. Removing an inaccurate derogatory mark can instantly boost your FICO score.

Sub-Action 2.3: Strategize on Old Derogatory Accounts

For legitimate but old derogatory accounts (collections, charge-offs), consider a ‘pay-for-delete’ negotiation. This is where you offer to pay a collection agency a portion of the debt in exchange for them agreeing to remove the negative entry from your credit report. This is not guaranteed, as collection agencies are not obligated to remove accurate information, but it’s worth attempting, especially for older debts. Always get any agreement in writing before making a payment.

Impact in 6 Months: Correcting errors can provide an immediate boost, sometimes quite substantial. Successfully negotiating a pay-for-delete can also significantly improve your score. This diligent monitoring and action are vital for comprehensive credit score optimization.

Action 3: Strategic Credit Building and Management (Long-Term Gains, Short-Term Benefits)

While payment history and utilization are quick wins, strategic credit building and management contribute to sustained credit score optimization and can provide incremental gains even within six months. This involves understanding the ‘length of credit history,’ ‘new credit,’ and ‘credit mix’ components.

Sub-Action 3.1: Become an Authorized User (If Applicable)

If you have a trusted family member or partner with an excellent, long-standing credit history, ask them to add you as an authorized user on one of their well-managed credit cards. Their positive payment history and low utilization will often be added to your credit report, potentially boosting your score. Ensure they maintain good habits, as their missteps could also affect you. This is a powerful, yet often overlooked, tactic for rapid credit score optimization.

Sub-Action 3.2: Consider a Secured Credit Card or Credit Builder Loan (If Needed)

If your credit history is thin or poor, a secured credit card or credit builder loan can be an excellent way to establish or re-establish positive credit. With a secured card, you provide a deposit that acts as your credit limit. With a credit builder loan, you make payments into a savings account, and once the loan is paid off, you receive the funds. Both report to credit bureaus, building a positive payment history.

Sub-Action 3.3: Avoid Unnecessary New Credit Applications

Each time you apply for new credit (a credit card, a loan, etc.), a ‘hard inquiry’ is placed on your credit report. While one or two inquiries won’t devastate your score, multiple inquiries in a short period can signal risk and temporarily lower your score. During your six-month push for credit score optimization, limit new credit applications unless absolutely necessary.

Sub-Action 3.4: Maintain a Healthy Credit Mix Over Time

While less impactful in the short term, having a mix of revolving credit (credit cards) and installment credit (loans) can be beneficial. If you only have credit cards, consider a small, manageable installment loan (like a personal loan for a specific purpose) if it makes financial sense and you can easily repay it. This demonstrates your ability to handle different types of debt responsibly. However, do not take on debt you don’t need solely for this purpose.

Impact in 6 Months: Becoming an authorized user can show immediate positive impact. Secured cards and credit builder loans take a few months to report and build history, contributing to steady gains. Avoiding new inquiries prevents unnecessary score drops. All these elements collectively support robust credit score optimization.

Putting It All Together: Your 6-Month Credit Score Optimization Plan

Here’s a snapshot of how to integrate these actions into a cohesive plan:

Month 1-2: Foundation and Immediate Impact

- Get Your Reports: Pull all three credit reports from AnnualCreditReport.com. Review them meticulously for errors.

- Set Up Auto-Payments: Ensure all recurring payments are automated.

- Aggressive Balance Reduction: Focus on paying down credit card balances, especially those with high utilization. Aim to get all utilization under 30%, ideally under 10%.

- Dispute Errors: File disputes for any inaccuracies found on your reports.

- Authorized User (If Possible): If you have a trusted individual, initiate this process.

Month 3-4: Sustain and Monitor

- Continue On-Time Payments: Maintain your perfect payment record.

- Keep Utilization Low: Resist the urge to spend on your credit cards. If you use them, pay them off immediately.

- Monitor Dispute Progress: Follow up on any disputes.

- Consider Secured Card/Credit Builder Loan: If your credit is very thin, initiate one of these.

- Avoid New Credit: Do not apply for any new loans or credit cards.

Month 5-6: Refine and Reinforce

- Review Progress: Pull one more credit report (from a bureau you haven’t recently checked) to see the progress of your disputes and payment history.

- Maintain Habits: Continue all the positive habits established.

- Final Utilization Push: If you’re close to your goal, make an extra effort to pay down balances before your statement closing dates.

- Celebrate Small Wins: Acknowledge the positive changes you’re making!

Common Pitfalls to Avoid During Credit Score Optimization

Even with the best intentions, certain actions can inadvertently harm your score. Be mindful of these:

- Closing Old Accounts: As mentioned, this can reduce your overall available credit and shorten your credit history, both detrimental to credit score optimization.

- Applying for Too Much New Credit: Multiple hard inquiries signal risk and can lower your average account age.

- Ignoring Small Debts: Even a small, forgotten medical bill sent to collections can have a significant negative impact. Don’t let anything slip through the cracks.

- Not Checking Your Reports: Assuming everything is accurate is a costly mistake. Regular monitoring is key to preventing and correcting issues.

- Expecting Instant Results: While some improvements can be quick, a 50-point jump requires consistent effort over several months. Patience and persistence are crucial.

Beyond 6 Months: Sustaining Your Optimized Credit Score

Achieving a 50-point increase in six months is a fantastic accomplishment, but credit score optimization is an ongoing process. To maintain and further improve your score:

- Continue On-Time Payments: This remains the most critical factor.

- Keep Utilization Low: Make it a habit to pay off credit card balances in full each month.

- Monitor Your Reports Annually: Keep checking for errors and fraudulent activity.

- Diversify Your Credit Mix Sensibly: As your financial needs evolve, having a healthy mix of credit types can be beneficial, but always avoid unnecessary debt.

- Build a Strong Emergency Fund: This reduces the likelihood of relying on credit cards for unexpected expenses, helping you maintain low utilization.

The Future of Credit Score Optimization in 2026 and Beyond

As we move further into 2026, credit scoring models may continue to evolve, incorporating new data points like banking transaction data (e.g., UltraFICO) or rent payment history (e.g., Experian Boost). While these newer models aim to be more inclusive, the core principles of FICO scoring – responsible payment behavior and judicious use of credit – will always remain paramount. Focusing on these fundamentals ensures your credit score optimization efforts are future-proof and effective regardless of minor model changes.

Conclusion: Take Control of Your Financial Future

Boosting your FICO score by 50 points in six months through dedicated credit score optimization is an achievable goal. By focusing on mastering your payments, drastically reducing credit utilization, and diligently monitoring and correcting your credit reports, you are taking powerful steps toward a healthier financial future. Remember, your credit score is a reflection of your financial habits, and with conscious effort, you can mold it to serve your goals. Start today, stay consistent, and watch your financial opportunities expand.