Maximize Your 2026 Social Security Benefits: Expert Strategies for a 2% Increase

The landscape of retirement planning is constantly evolving, and a critical component for many Americans is understanding and maximizing their Social Security benefits. As we look towards 2026, the prospect of a 2% increase in payments, or even more, is a significant consideration for current and future retirees. This comprehensive guide delves into the intricacies of the Social Security system, offering expert tips and actionable strategies to help you navigate the complexities and potentially boost your 2026 Social Security benefits.

For millions, Social Security represents a foundational pillar of financial security in retirement. However, simply receiving benefits isn’t enough; maximizing them requires a proactive approach and a deep understanding of the factors that influence your monthly payments. From the annual Cost-of-Living Adjustment (COLA) to strategic claiming decisions and meticulous record-keeping, every detail can contribute to a more robust retirement income. Our focus here is on empowering you with the knowledge to make informed choices that can lead to a tangible increase in your 2026 Social Security benefits.

The journey to optimizing your Social Security payments begins with education. Many people approach retirement without fully grasping the nuances of how their benefits are calculated or the various options available to them. This can lead to leaving money on the table, which could otherwise significantly impact their quality of life during their golden years. By exploring the key elements that determine your benefit amount and understanding the potential for adjustments, you can position yourself to not only receive your due but to actively seek out opportunities for enhancement.

Understanding the Foundation: How Social Security Benefits are Calculated

Before we can talk about increasing your 2026 Social Security benefits, it’s essential to grasp the fundamental principles behind their calculation. Your Social Security benefit is not a fixed amount; it’s a personalized figure based on your lifetime earnings. The Social Security Administration (SSA) calculates your benefit using a formula that considers your 35 highest-earning years. If you have fewer than 35 years of earnings, the missing years are counted as zero, which can significantly reduce your average earnings and, consequently, your benefit amount.

Average Indexed Monthly Earnings (AIME)

The first step in the calculation is determining your Average Indexed Monthly Earnings (AIME). Your earnings from past years are ‘indexed’ to account for changes in average wages in the economy. This indexing ensures that your past earnings are expressed in terms of their current value, making them comparable to today’s wages. For example, earnings from 1980 will be adjusted upwards to reflect the general increase in wages since then. Only earnings up to the annual Social Security taxable maximum are considered.

Primary Insurance Amount (PIA)

Once your AIME is calculated, the SSA applies a progressive formula to arrive at your Primary Insurance Amount (PIA). The PIA is the benefit you’re entitled to if you claim at your Full Retirement Age (FRA). The formula uses ‘bend points’ – specific dollar amounts that divide your AIME into segments. Different percentages are applied to each segment, with lower segments receiving a higher percentage. This progressive structure means that lower-income earners receive a higher percentage of their average indexed earnings back in benefits compared to higher-income earners. Understanding your PIA is crucial because it forms the baseline for all subsequent adjustments, whether due to early claiming, delayed claiming, or COLA.

Factors Influencing Your Initial Benefit

- Years of Work: As mentioned, 35 years of earnings are used. Working more than 35 years can replace lower-earning years with higher-earning ones, increasing your AIME.

- Earning History: The higher your indexed earnings over your career, up to the taxable maximum, the higher your AIME and, consequently, your PIA.

- Full Retirement Age (FRA): This is the age at which you’re eligible to receive 100% of your PIA. FRA varies based on your birth year. For those born in 1960 or later, FRA is 67.

Having a solid understanding of these foundational elements is the first step toward strategically positioning yourself for higher 2026 Social Security benefits. It highlights the importance of consistent employment and maximizing your earnings throughout your working life, as these directly impact the core calculation of your retirement income.

The Power of COLA: A Key Driver for 2026 Social Security Benefits

One of the most significant factors influencing your annual Social Security payments, including your 2026 Social Security benefits, is the Cost-of-Living Adjustment (COLA). COLA is an annual increase in benefits designed to offset the effects of inflation, ensuring that the purchasing power of your benefits doesn’t erode over time. While the exact percentage of the 2026 COLA won’t be announced until late 2025, understanding how it’s determined can help you anticipate potential adjustments and plan accordingly.

How COLA is Determined

COLA is calculated based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Specifically, the average CPI-W for the third quarter (July, August, and September) of the current year is compared to the average CPI-W for the third quarter of the most recent year in which a COLA was payable. If there’s an increase, that percentage increase (rounded to the nearest one-tenth of one percent) becomes the COLA for the following year. For example, the 2025 COLA will be based on the CPI-W from Q3 2024. Therefore, the 2026 COLA will be determined by comparing Q3 2025 CPI-W data to Q3 2024 CPI-W data.

Historical COLA Trends and Future Projections

Historically, COLA percentages have varied widely, reflecting economic conditions and inflation rates. In years with high inflation, COLA has been substantial, providing a significant boost to benefits. In periods of low inflation, COLA has been minimal or even zero. While no one can predict the future with absolute certainty, economic forecasts and inflation trends provide clues. For example, if inflation remains elevated in 2025, it’s reasonable to expect a noticeable COLA for 2026. Conversely, a period of disinflation could lead to a smaller COLA.

A 2% increase in 2026 Social Security benefits due to COLA would be a welcome adjustment for many retirees. While it’s not a guaranteed figure, it’s a realistic possibility given historical averages and ongoing economic dynamics. Monitoring inflation reports and economic projections from reputable sources can give you an early indication of what to expect for your 2026 Social Security benefits.

The Impact of COLA on Your Long-Term Financial Health

The cumulative effect of COLA over many years can be profound. Even seemingly small annual adjustments add up, helping to preserve your purchasing power throughout a potentially long retirement. Without COLA, the real value of your fixed Social Security income would steadily decline due to inflation, making it harder to cover living expenses. Therefore, understanding and factoring in COLA projections, even if they are estimates, is a crucial part of long-term retirement planning and managing your 2026 Social Security benefits effectively.

Strategic Claiming: When to Start Receiving Your 2026 Social Security Benefits

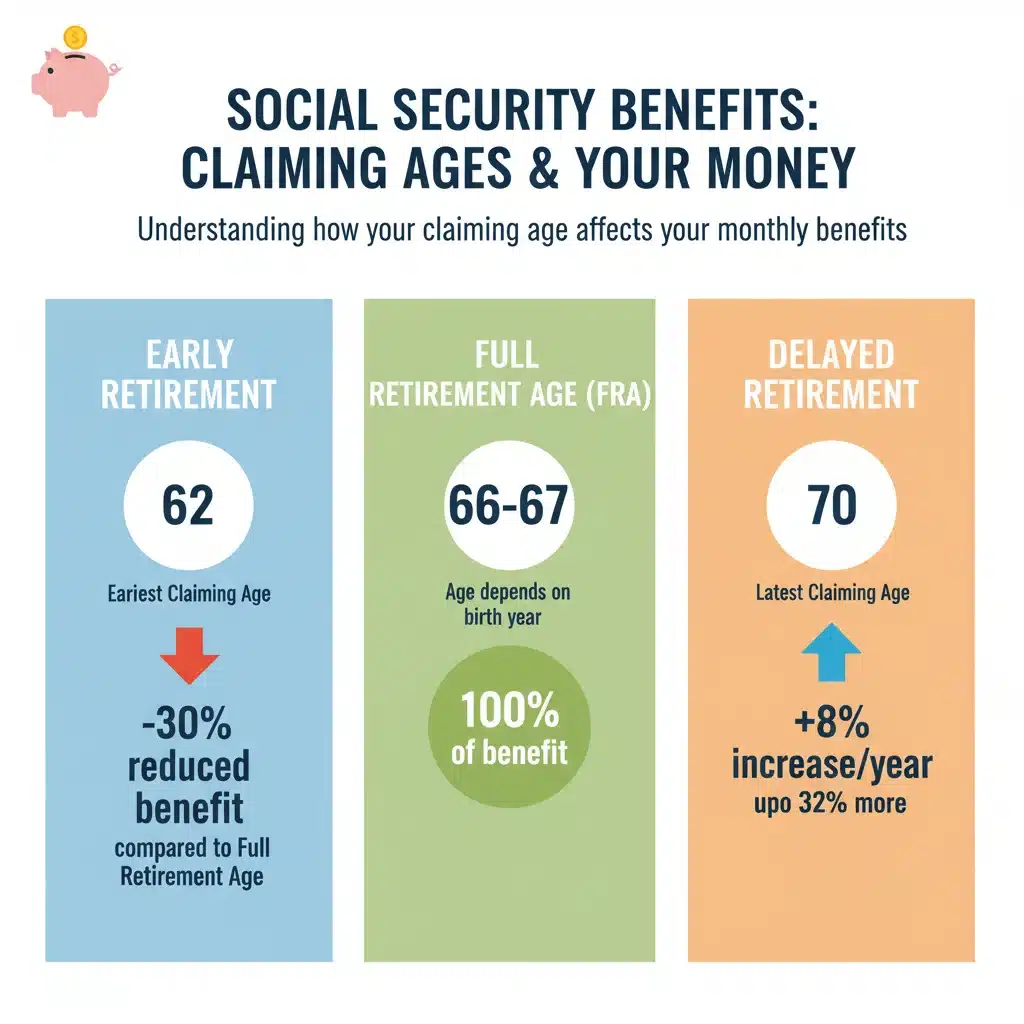

Perhaps one of the most impactful decisions you’ll make regarding your 2026 Social Security benefits is *when* to start claiming them. This decision alone can significantly alter your monthly payment for the rest of your life. While you can claim benefits as early as age 62, or delay them until age 70, each option comes with its own set of advantages and disadvantages.

Early Claiming (Age 62)

Claiming at age 62, the earliest possible age, means you’ll receive benefits for a longer period. However, your monthly payment will be permanently reduced. The reduction can be substantial, often around 25-30% of your Full Retirement Age (FRA) benefit, depending on your birth year. For example, if your FRA is 67, claiming at 62 would result in a 30% reduction. While this might seem appealing for immediate income, it’s crucial to consider the long-term financial implications. If you expect to live a long life, the cumulative reduction could mean leaving a significant amount of money on the table over your retirement.

Full Retirement Age (FRA) Claiming

Claiming at your Full Retirement Age (FRA) means you receive 100% of your Primary Insurance Amount (PIA). As mentioned, your FRA depends on your birth year. For those born in 1960 or later, FRA is 67. This is often considered the baseline for comparison. If you’re able to work until your FRA, or have other income sources to bridge the gap, claiming at this age ensures you receive your full earned benefit without any reductions for early claiming.

Delayed Claiming (Up to Age 70)

For every year you delay claiming benefits past your FRA, up until age 70, you earn Delayed Retirement Credits (DRCs). These credits result in an increase of approximately 8% per year (or two-thirds of 1% per month) on your monthly benefit. This increase is permanent and applies to your initial benefit amount, which will then also be subject to future COLA adjustments. For someone with an FRA of 67, delaying until 70 could result in a 24% increase over their FRA benefit. This strategy is particularly powerful for those who are in good health, have sufficient savings to cover expenses in their early retirement years, or continue to work.

Factors to Consider When Deciding Your Claiming Age:

- Life Expectancy: If you anticipate a longer lifespan, delaying benefits often makes financial sense due to the higher monthly payments.

- Current Health: Poor health or a family history of shorter lifespans might make early claiming a more suitable option.

- Other Income Sources: Do you have a pension, 401(k), IRA, or other savings to draw upon if you delay Social Security?

- Need for Income: Do you need the income immediately to cover living expenses?

- Spousal Benefits: The claiming decision of one spouse can significantly impact the other’s benefits, especially survivor benefits.

The decision of when to claim your 2026 Social Security benefits is highly personal and should be made after careful consideration of your individual circumstances. Consulting with a financial advisor specializing in Social Security can provide personalized insights and help you project the long-term impact of your choices.

Optimizing Your Earnings Record: A Direct Path to Higher 2026 Social Security Benefits

Your lifetime earnings record is the bedrock upon which your Social Security benefits are built. The more you earn (up to the annual taxable maximum) and the longer you work, the higher your potential benefits. This direct correlation makes optimizing your earnings record a crucial strategy for increasing your 2026 Social Security benefits.

Working Longer and Earning More

As established, the SSA uses your 35 highest-earning years to calculate your benefit. If you’ve worked fewer than 35 years, every additional year you work at a decent salary will replace a zero-earning year, significantly boosting your average indexed monthly earnings (AIME). Even if you have 35 years of earnings, continuing to work can replace one of your lower-earning years with a higher-earning one, further increasing your AIME and, consequently, your Primary Insurance Amount (PIA).

For example, if you had a few years in your early career with very low earnings, working a few more years at a higher salary just before retirement can have a disproportionately positive effect on your overall benefit calculation. This is a simple yet powerful strategy to directly impact your 2026 Social Security benefits.

Verifying Your Earnings Record Annually

Errors in your earnings record, though rare, can happen. Employers might make mistakes in reporting your wages, or there could be data entry errors at the SSA. Such errors, if uncorrected, could lead to a lower benefit payment than you’re rightfully owed. Therefore, it’s absolutely critical to regularly review your Social Security earnings statement.

You can access your Social Security statement online by creating an account at ssa.gov. This statement provides a detailed history of your reported earnings year by year. It also gives you an estimate of your future benefits based on your current earnings record. Review this statement at least once a year to ensure all your earnings are accurately reported. If you find any discrepancies, contact the SSA immediately with supporting documentation, such as W-2 forms or tax returns, to get them corrected.

Understanding the Taxable Maximum

It’s important to remember that Social Security only taxes and credits earnings up to a certain annual limit, known as the Social Security taxable maximum. For 2024, this limit is $168,600. Earnings above this amount are not subject to Social Security taxes and do not count towards your benefit calculation. While earning more than the taxable maximum won’t directly increase your Social Security benefit further, working up to and consistently reaching this maximum for 35 years will result in the highest possible benefit.

By actively managing and verifying your earnings record, you’re not just being diligent; you’re taking concrete steps to ensure your 2026 Social Security benefits accurately reflect your contributions and are as high as they can be based on your work history.

Navigating Spousal and Survivor Benefits for Enhanced 2026 Social Security Benefits

Social Security isn’t just about individual benefits; it also provides crucial financial support for families through spousal and survivor benefits. Understanding these provisions can be a powerful strategy for maximizing your household’s overall 2026 Social Security benefits, especially for couples or surviving family members.

Spousal Benefits

If you are married, divorced, or widowed, you may be eligible for benefits based on your spouse’s (or ex-spouse’s) earnings record, even if you haven’t worked or have a very limited work history. Spousal benefits can be up to 50% of your spouse’s Full Retirement Age (PIA) amount. To claim spousal benefits, your spouse must have already claimed their own retirement benefits. The earliest you can claim spousal benefits is age 62, but like individual benefits, they will be reduced if claimed before your own Full Retirement Age (FRA).

A key strategy for couples is to coordinate their claiming decisions. For instance, if one spouse has a significantly higher earnings record, they might consider delaying their benefits until age 70 to maximize their payment (and potentially the survivor benefit). The lower-earning spouse could claim their own (reduced) benefit, or a spousal benefit, earlier, providing some income while the higher earner’s benefit grows. This complex decision often benefits from professional financial advice to model different scenarios and determine the optimal strategy for maximizing combined 2026 Social Security benefits.

Divorced Spouse Benefits

Even if you’re divorced, you may still be eligible for benefits based on your ex-spouse’s record. To qualify, your marriage must have lasted at least 10 years, you must be at least 62 years old, you must be currently unmarried, and your ex-spouse must be entitled to Social Security retirement or disability benefits. If your ex-spouse is eligible for benefits but hasn’t yet claimed them, you can still claim benefits on their record if you’ve been divorced for at least two years. The amount you receive as a divorced spouse will not affect the benefits your ex-spouse or their current spouse receives.

Survivor Benefits

Survivor benefits are paid to eligible family members of a deceased worker. This can include a widow or widower, divorced widow or widower, children, or dependent parents. The amount of the survivor benefit depends on the deceased worker’s earnings record and the age of the survivor when they claim. A surviving spouse can receive up to 100% of the deceased worker’s basic Social Security benefit if they claim at their own Full Retirement Age for survivor benefits (which may be different from their FRA for retirement benefits) or older. Claiming earlier will result in a reduced benefit.

For widows and widowers, a common strategy is to claim one type of benefit (e.g., survivor benefits) first and then switch to their own retirement benefit later if their own benefit will be higher due to delayed retirement credits. This allows one benefit to grow while the other provides income. Understanding these intricate rules is paramount for ensuring you and your family receive all the 2026 Social Security benefits you are entitled to.

Beyond the Basics: Advanced Strategies for Boosting Your 2026 Social Security Benefits

While understanding COLA, claiming age, and earnings records forms the core of maximizing your 2026 Social Security benefits, several advanced strategies can further enhance your retirement income. These often require careful planning and a nuanced understanding of Social Security rules.

Minimizing Taxation of Benefits

A portion of your Social Security benefits may be taxable, depending on your ‘provisional income.’ Provisional income includes your adjusted gross income (AGI), tax-exempt interest, and one-half of your Social Security benefits. If your provisional income exceeds certain thresholds, up to 85% of your Social Security benefits can become taxable. While this doesn’t directly increase your benefit payment, reducing your tax liability on those benefits effectively increases your net income from Social Security.

Strategies to consider include:

- Strategic Roth Conversions: Converting traditional IRA or 401(k) funds to a Roth account in lower-income years before retirement can reduce future Required Minimum Distributions (RMDs) from pre-tax accounts, which contribute to provisional income.

- Qualified Charitable Distributions (QCDs): If you’re over 70½, you can donate directly from your IRA to a charity. This reduces your taxable IRA distribution, lowers your AGI, and consequently, your provisional income, potentially reducing the taxation of your Social Security benefits.

- Managing Other Retirement Withdrawals: Coordinating withdrawals from different types of retirement accounts (taxable, tax-deferred, tax-free) can help manage your provisional income in retirement.

Working While Receiving Benefits: The Earnings Test

If you claim Social Security benefits before your Full Retirement Age (FRA) and continue to work, your benefits may be reduced if your earnings exceed certain annual limits. This is known as the ‘earnings test.’ For 2024, if you are under FRA for the entire year, the SSA deducts $1 from your benefits for every $2 you earn above $22,320. In the year you reach FRA, the deduction is $1 for every $3 earned above a higher limit ($59,520 in 2024) until the month you reach FRA. Once you reach your FRA, the earnings test no longer applies, and you can earn as much as you want without your benefits being reduced.

It’s important to note that any benefits withheld due to the earnings test are not lost permanently. When you reach your FRA, your monthly benefit will be recalculated to account for the withheld benefits, effectively increasing your future payments. However, being aware of the earnings test is crucial for planning your work and claiming strategy to ensure you’re maximizing your 2026 Social Security benefits without unexpected reductions.

Understanding the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO)

If you receive a pension from a job where you did not pay Social Security taxes (e.g., some government jobs, foreign employment), your Social Security benefits (WEP) or spousal/survivor benefits (GPO) may be reduced. These provisions are complex and can significantly impact your benefits. If you fall into these categories, it’s essential to understand how WEP and GPO apply to your specific situation and factor them into your retirement planning for your 2026 Social Security benefits.

Consulting with a Social Security Expert

Given the complexity and personalized nature of Social Security planning, consulting with a financial advisor who specializes in Social Security can be invaluable. They can help you:

- Project your benefits under various claiming scenarios.

- Analyze the impact of different strategies on your overall retirement income.

- Navigate spousal and survivor benefit rules.

- Understand and address potential issues like the earnings test, WEP, or GPO.

Their expertise can help you avoid costly mistakes and ensure you’re truly maximizing your 2026 Social Security benefits to support your retirement goals.

Future Outlook and Staying Informed for Your 2026 Social Security Benefits

The Social Security system is dynamic, influenced by economic, demographic, and legislative factors. Staying informed about potential changes is crucial for effective long-term planning for your 2026 Social Security benefits and beyond.

Potential Legislative Changes

Social Security faces long-term financial challenges, and there are ongoing discussions in Congress about potential reforms. These could include adjustments to the Full Retirement Age, changes to the COLA calculation, modifications to the benefit formula, or increases in the Social Security payroll tax cap. While significant legislative changes are often difficult to pass, it’s wise to be aware of the ongoing dialogue and how proposed changes might impact your future benefits. Reputable financial news sources and the SSA website (ssa.gov) are excellent resources for staying updated.

Economic Indicators and COLA Projections

As discussed, COLA is directly tied to inflation. Keeping an eye on economic indicators like the Consumer Price Index (CPI) and wage growth can provide early clues about the potential for future COLAs. While the SSA officially announces the COLA in October each year for the following year, economists and financial analysts often publish projections well in advance. These projections, while not guarantees, can help you in your financial planning for your 2026 Social Security benefits.

Regularly Reviewing Your Social Security Statement

We’ve emphasized this before, but it bears repeating: regularly review your Social Security statement. This document provides not only your earnings history but also personalized estimates of your future benefits under different claiming scenarios. As your earnings change, or as you get closer to retirement, these estimates will be updated, providing the most current information for your planning. An accurate statement is the foundation for accurate benefit projections and maximizing your 2026 Social Security benefits.

Continuous Learning and Adaptation

Retirement planning is not a one-time event; it’s an ongoing process. As your life circumstances change (e.g., marriage, divorce, new job, health changes), your Social Security strategy may need to adapt. Continuously educating yourself about Social Security rules, consulting with financial professionals, and reviewing your overall retirement plan will ensure that you remain on the optimal path for maximizing your 2026 Social Security benefits and securing your financial future.

By taking a proactive, informed, and strategic approach, you can significantly influence the amount of your 2026 Social Security benefits, transforming what might seem like a fixed payment into a flexible asset that can be optimized for your long-term well-being. The effort you put into understanding and planning for Social Security today will yield substantial rewards in your retirement years.

")

& IRA Strategies for 2025")

in 2026: A Guide to the New $23,000 Limit")