2026 Housing Market Forecast: Why Home Prices May See a 2% Correction

The real estate landscape is perpetually in motion, a dynamic interplay of economic forces, demographic shifts, and market sentiment. As we cast our gaze towards the future, specifically the year 2026, a nuanced picture begins to emerge for the housing market. While predictions are inherently challenging, a growing consensus among economists and real estate analysts suggests a potential 2% correction in home prices. This isn’t a call for panic, but rather an invitation for informed understanding and strategic planning. This comprehensive analysis will delve into the intricate factors contributing to this 2026 housing forecast, examining the underlying economic currents, the role of interest rates, supply and demand dynamics, and the regional variations that will define the market in the coming years.

Understanding the 2026 housing forecast requires a multi-faceted approach. We will explore the macroeconomic indicators that influence housing, such as inflation, employment rates, and GDP growth. Furthermore, we will dissect the impact of monetary policy, particularly the trajectory of interest rates, which directly affects affordability and buyer demand. The delicate balance between housing supply and demand will also be a critical component of our discussion, as will the evolving preferences of homebuyers and sellers. Finally, we will consider the regional disparities that often characterize the U.S. housing market, providing a more localized perspective on the anticipated correction. Whether you are a prospective homebuyer, a current homeowner, a real estate investor, or simply an interested observer, this in-depth exploration aims to equip you with the knowledge needed to navigate the evolving real estate terrain of 2026.

The Macroeconomic Undercurrents Shaping the 2026 Housing Forecast

To comprehend the projected 2% correction in home prices for the 2026 housing forecast, it’s imperative to first understand the broader macroeconomic environment. The health of the overall economy is inextricably linked to the performance of the housing market. Several key economic indicators will play a pivotal role in shaping the trajectory of home prices in the coming years.

Inflation and its Ripple Effects

Inflation, while showing signs of moderation, remains a significant factor. Persistent inflation can erode purchasing power, making it more challenging for potential homebuyers to afford rising home prices and higher mortgage payments. The Federal Reserve’s response to inflation, primarily through interest rate adjustments, directly impacts borrowing costs. If inflation remains stubbornly high, the Fed may be compelled to maintain a hawkish stance, keeping interest rates elevated, which could further dampen housing demand and contribute to a price correction. Conversely, a sustained decline in inflation could provide the Fed with room to ease monetary policy, potentially stimulating the market.

Employment and Wage Growth

A robust job market with consistent wage growth is typically a strong tailwind for the housing market. When people feel secure in their employment and see their incomes rising, they are more confident in making large financial commitments like purchasing a home. However, if there are signs of a slowdown in employment growth or a significant increase in unemployment, consumer confidence could wane, leading to a decrease in buyer activity. The current labor market, while strong in many sectors, faces potential headwinds from technological advancements and global economic shifts. Monitoring these trends will be crucial for understanding the demand side of the 2026 housing forecast.

Gross Domestic Product (GDP) Growth

GDP growth serves as a broad measure of economic activity. A healthy and expanding economy generally supports a strong housing market. When the economy is growing, businesses expand, jobs are created, and overall wealth increases, all of which contribute to a greater capacity for homeownership. Conversely, a sluggish or contracting GDP could signal an economic downturn, which historically has corresponded with a cooling or correcting housing market. The pace of economic recovery and expansion post-pandemic, coupled with potential global economic uncertainties, will undoubtedly influence the strength of the housing sector in 2026.

The interplay of these macroeconomic factors creates a complex web of influences on the housing market. A slight recalibration in any one of these areas can have cascading effects, ultimately contributing to the projected 2% correction in home prices. It’s not about a single trigger, but rather a confluence of forces that will collectively shape the 2026 housing forecast.

The Pivotal Role of Interest Rates in the 2026 Housing Forecast

Perhaps no single factor exerts as much immediate influence on the housing market as interest rates. The cost of borrowing directly impacts affordability, and even small fluctuations can have significant consequences for potential homebuyers. The Federal Reserve’s monetary policy decisions, particularly regarding the federal funds rate, ripple through the economy to affect mortgage rates.

The Trajectory of Mortgage Rates

The recent period has seen a notable increase in mortgage rates from historical lows. This upward trend has already had a cooling effect on the market, pricing out some buyers and reducing overall purchasing power. For the 2026 housing forecast, the key question is whether mortgage rates will stabilize, continue to rise, or begin to recede. If inflation proves to be more persistent than anticipated, the Fed may be forced to keep interest rates higher for longer, leading to sustained elevated mortgage rates. This scenario would likely continue to put downward pressure on home prices as affordability remains a challenge for a larger segment of the population.

Conversely, if inflation cools more rapidly and the economy shows signs of slowing, the Fed might consider cutting interest rates. Lower interest rates would make mortgages more affordable, potentially stimulating demand and mitigating the extent of any price correction. However, a significant drop in rates is not widely anticipated in the near term, given the Fed’s commitment to price stability.

Affordability Crisis and Buyer Behavior

High interest rates, combined with elevated home prices, have created an affordability crisis in many markets across the country. This crisis is a primary driver behind the anticipated 2% correction in the 2026 housing forecast. When homes become too expensive relative to average incomes and borrowing costs, demand naturally wanes. Potential buyers are either priced out entirely or choose to delay their purchase, hoping for more favorable market conditions.

This shift in buyer behavior is crucial. A reduction in the pool of eligible buyers means less competition for available homes, which can lead to longer market times and, eventually, price adjustments. Furthermore, the psychological impact of higher rates can also play a role, as potential buyers may feel less enthusiastic about entering a market where their monthly payments are significantly higher than they would have been just a few years prior. The balance between what buyers are willing and able to pay will be a defining characteristic of the 2026 market.

Supply and Demand Dynamics: A Balancing Act in the 2026 Housing Forecast

The fundamental economic principles of supply and demand are always at play in the housing market. For the 2026 housing forecast, the interaction between the number of available homes and the pool of interested buyers will be critical in determining the extent and nature of any price correction.

Current Inventory Levels

For several years, many housing markets have struggled with chronically low inventory. A shortage of homes for sale, coupled with robust demand, was a significant factor in the rapid appreciation of home prices. However, as interest rates have risen and demand has softened, inventory levels have begun to tick up in some areas. While still below historical averages in many regions, an increase in available homes can provide buyers with more options and reduce the urgency to bid up prices.

The pace at which new inventory comes onto the market will be a key determinant for the 2026 housing forecast. If more homeowners choose to sell, either due to changing life circumstances or a desire to capitalize on remaining equity, and if new construction continues to add to the housing stock, the supply side of the equation could exert further downward pressure on prices.

New Construction and Development

The rate of new home construction is another vital piece of the supply puzzle. While builders have faced challenges with labor shortages and supply chain disruptions, there has been a concerted effort to increase housing starts in many areas. However, the cost of materials and labor, coupled with higher interest rates for construction loans, can still constrain the pace of new development. The ability of builders to deliver more affordable housing options will be particularly important in addressing the overall affordability crisis and influencing the 2026 housing forecast.

Demographic Shifts and Buyer Preferences

Demographic trends continue to shape housing demand. The large millennial generation, now in their prime homebuying years, represents a significant source of potential demand. However, their ability to enter the market is heavily influenced by affordability. Gen Z is also beginning to enter the housing market, albeit in smaller numbers, and their preferences for location, home size, and amenities will evolve over time.

Furthermore, evolving work-from-home trends continue to influence where people choose to live, potentially driving demand in more suburban or rural areas and shifting preferences away from traditional urban centers. These demographic shifts, coupled with changing buyer preferences for sustainability, technology, and community, will add another layer of complexity to the supply and demand dynamics of the 2026 housing forecast.

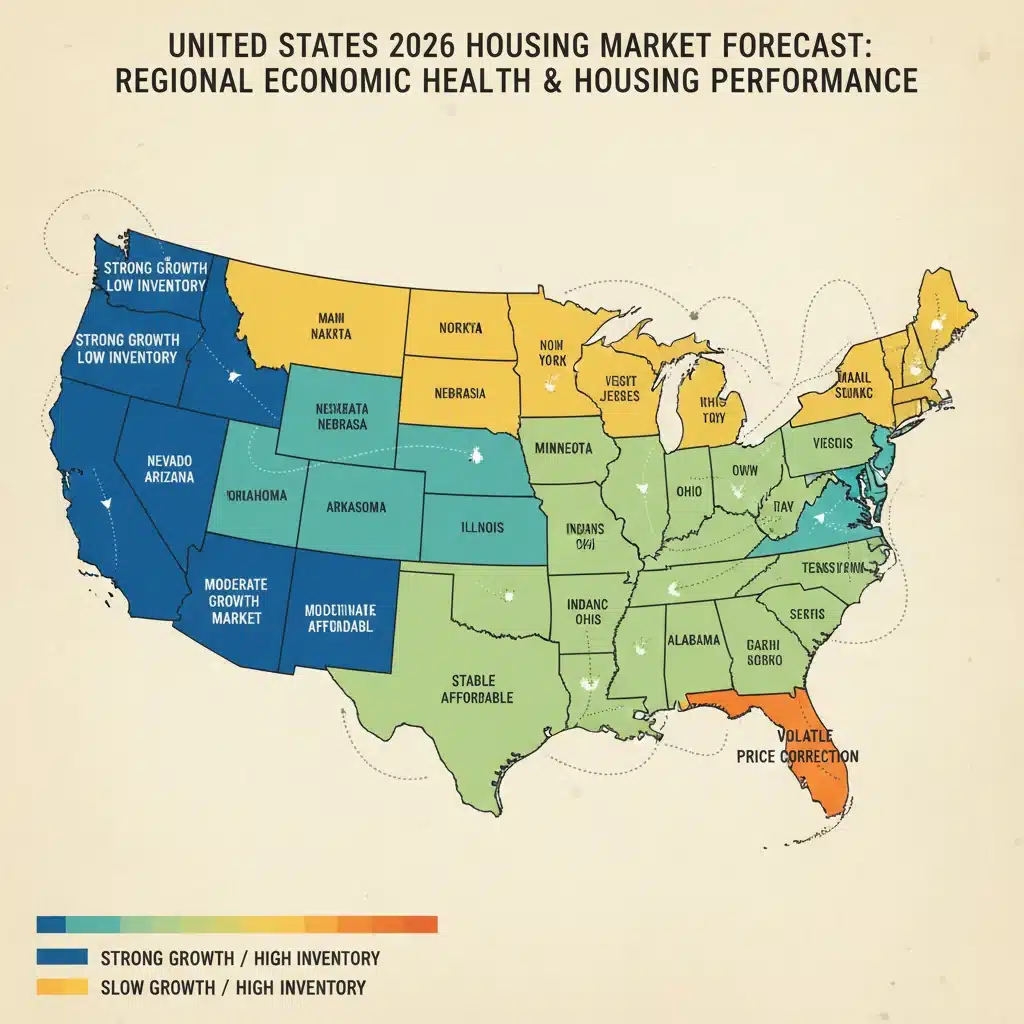

Regional Variations: A Patchwork of Performance in the 2026 Housing Forecast

It is crucial to remember that the U.S. housing market is not a monolith. While national averages and forecasts provide a general overview, real estate is inherently local. The 2% correction projected for the 2026 housing forecast will likely manifest differently across various regions, with some areas experiencing more significant adjustments and others remaining relatively stable or even continuing to see modest growth.

Boom and Bust Regions

During the recent housing boom, certain markets experienced exponential price growth, often fueled by inward migration, strong job markets, and limited supply. These ‘boom’ regions, particularly those in the Sun Belt and intermountain West, may be more susceptible to price corrections as affordability becomes stretched and out-of-state buyers face higher borrowing costs. Markets that saw the most aggressive price appreciation are often the first to see a correction when market conditions shift. Conversely, historically stable and less volatile markets may see more muted adjustments.

Economic Diversification and Local Job Markets

The economic health and diversification of a local job market play a significant role in its housing market’s resilience. Regions with diverse industries and strong, growing employment opportunities tend to weather economic downturns better than those reliant on a single industry. For the 2026 housing forecast, areas with robust tech sectors, healthcare industries, or strong manufacturing bases may see more sustained demand, even if at a slower pace. Conversely, regions experiencing job losses or economic stagnation could face more pronounced housing market challenges.

Population Growth and Migration Patterns

Population growth and migration patterns continue to be powerful drivers of local housing demand. Areas that continue to attract new residents, either due to job opportunities, lower cost of living, or desirable lifestyles, are likely to maintain stronger housing markets. However, if these migration patterns shift, or if the influx of new residents slows, it could impact local housing demand. The interplay between remote work policies and migration will continue to be a fascinating aspect of the 2026 housing forecast.

Regulatory Environment and Housing Policy

Local and state regulations, including zoning laws, building codes, and permitting processes, can significantly influence housing supply and affordability. Regions with more restrictive policies often face greater supply constraints, which can exacerbate price increases during booms and limit the speed of recovery during downturns. Changes in housing policy, or a concerted effort to streamline development in some areas, could also impact the local housing market dynamics leading up to and during 2026.

Therefore, while a national 2% correction is a useful benchmark for the 2026 housing forecast, it’s essential for individuals to research and understand the specific conditions of their local market. What happens in one city or state may not necessarily reflect the experience in another, making localized analysis paramount for informed decision-making.

Implications for Buyers, Sellers, and Investors in the 2026 Housing Forecast

A projected 2% correction in home prices, as outlined in the 2026 housing forecast, carries distinct implications for different participants in the real estate market. Understanding these potential impacts can help individuals and businesses make more informed decisions.

For Prospective Homebuyers

For those looking to purchase a home, a 2% correction could offer a glimmer of hope for improved affordability. While not a dramatic drop, any reduction in home prices, coupled with potentially stable or slightly declining interest rates, could make homeownership more attainable. Buyers in 2026 may find themselves with slightly more negotiating power, longer market times for properties, and a greater selection of homes to choose from. However, it’s crucial for buyers to remain realistic; a 2% correction does not equate to a ‘buyer’s market’ in the traditional sense, but rather a less frenzied and potentially more balanced environment than recent years. Due diligence, pre-approval for mortgages, and a clear understanding of personal financial capacity will remain paramount.

For Current Homeowners and Potential Sellers

Current homeowners considering selling in 2026 should adjust their expectations. The days of multiple, over-asking-price offers within hours of listing may become less common. A 2% correction suggests a more normalized market where pricing strategies become even more critical. Sellers will need to ensure their homes are well-maintained, competitively priced, and effectively marketed to stand out. Those who purchased at the peak of the market might find their equity gains slightly diminished, but for most long-term homeowners, a 2% correction is unlikely to erase significant equity built over years. Strategic timing and working with experienced real estate professionals will be key for sellers navigating the 2026 housing forecast.

For Real Estate Investors

Real estate investors will need to approach the 2026 housing forecast with a refined strategy. A 2% correction could present opportunities for savvy investors to acquire properties at slightly more favorable prices, particularly in markets that experienced significant overvaluation. However, the cost of capital (interest rates) will remain a critical factor in determining profitability for rental properties or fix-and-flip projects. Investors will need to conduct thorough market analysis, focusing on cash flow, rental yields, and long-term appreciation potential rather than relying solely on rapid short-term gains. Diversification across different property types and geographic regions could also be a wise approach.

The Broader Economic Impact

A modest 2% correction is unlikely to trigger a widespread economic crisis. Instead, it could be seen as a healthy market recalibration, bringing prices back into better alignment with fundamental economic factors. This could alleviate some of the inflationary pressures associated with housing and potentially contribute to overall economic stability. However, the psychological impact on consumer confidence, particularly if the correction is uneven or more pronounced in certain areas, will be something to monitor closely as the 2026 housing forecast unfolds.

Navigating the 2026 Housing Market: Strategies and Outlook

As we look towards the 2026 housing forecast and the potential 2% correction in home prices, it’s clear that adaptability and informed decision-making will be paramount for all market participants. While the immediate future may bring some adjustments, the long-term outlook for real estate remains generally positive, underpinned by fundamental demand drivers.

Key Takeaways for the Future

- Moderation, Not Collapse: The projected 2% correction is a sign of market moderation, not a crash. It reflects a natural rebalancing after a period of rapid growth, influenced by higher interest rates and affordability challenges.

- Interest Rates Remain Central: The trajectory of inflation and the Federal Reserve’s response will continue to dictate interest rate movements, which in turn will heavily influence housing affordability and demand.

- Local Markets Reign Supreme: National forecasts provide a general direction, but real estate is inherently local. Understanding specific regional and neighborhood dynamics will be crucial for making sound decisions.

- Affordability is Key: The ongoing challenge of affordability will shape buyer behavior and continue to be a primary driver of market adjustments.

- Strategic Planning is Essential: Whether buying, selling, or investing, a well-thought-out strategy, based on current market conditions and future projections, will be vital for success.

Advice for Market Participants

For Buyers: Patience may be a virtue. Continue to save, improve your credit score, and get pre-approved. Be prepared to act when the right opportunity arises, but don’t feel pressured to overpay. Focus on properties that align with your long-term financial goals and lifestyle needs. A slightly less competitive market in 2026 could allow for more careful consideration and negotiation.

For Sellers: Prepare your home meticulously. Price it realistically based on comparable sales and current market conditions, not on peak-market exuberance. Be responsive to feedback and willing to negotiate. Understanding that the market has shifted from a seller’s advantage to a more balanced playing field will be crucial for a successful sale.

For Investors: Conduct thorough due diligence. Focus on markets with strong underlying economic fundamentals, population growth, and diversified job opportunities. Consider long-term rental strategies over short-term flips, given the potential for slower appreciation. Analyze cash flow and ensure your investment aligns with your risk tolerance and financial objectives.

The 2026 housing forecast, with its anticipated 2% correction, signals a return to a more rational and sustainable housing market. While it may not offer the dramatic opportunities or challenges of previous cycles, it demands a thoughtful and informed approach. By staying abreast of economic indicators, understanding local market nuances, and employing sound financial strategies, individuals can successfully navigate the evolving real estate landscape in the years to come. The goal is not to predict every twist and turn, but to be prepared for the general direction and its implications, ensuring resilience and capitalizing on opportunities as they arise.